Product Development

Chinese biotechs test the waters of novel technology platforms

Few platform companies are attracting top funding in China — at least not yet

Few platform companies are attracting top funding in China, but as the Chinese biotech sector evolves, it’s sampling new technologies through product licensing deals.

The Chinese biotechs attracting the most funding are accessing a growing number of innovative products through licensing deals, but so far, few have taken on the risk of developing technology platforms in-house. That picture could soon change.

BioCentury’s analysis of the 97 Chinese biotechs that have raised over $100 million in venture funding or at least $100 million in an IPO since 2014 shows that most of these companies are innovating on targets rather than technologies. Only 12 are technology platform companies.

As the sector continues to shift from generics, biosimilars and me-too products towards globally competitive innovative pipelines, the biggest fund-raisers are those building deep and diverse pipelines focused on new targets or new indications for established targets, but primarily within the realm small molecules and antibodies.

Platform companies in China have yet to attract the same level of funding as Western platform developers or domestic players with big portfolios.

But there’s evidence the Chinese biotech sector is moving in that direction.

Some of the most recent mega venture rounds have gone to novel platform plays. An example is CAR T developer CARsgen Therapeutics Co. Ltd., which raised $186 million in a November series C round that brought its total venturing funding to nearly $280 million.

Another CAR T company, JW Therapeutics Co. Ltd. (HKEX:2126), raised nearly $300 million in an IPO on the same day.

An analysis by BioCentury of in-licensing deals by China’s top funding magnets suggests the companies are testing the waters of new modalities such as cell therapies, bispecifics and next-generation antibodies by bringing in individual products generated by novel technology platforms.

Platforms were defined as new modalities and technologies that add novel features to existing modalities, such as next-generation antibody platforms.

China’s innovative target push

While most of China’s top fund-raisers do have generics, biosimilars and me-too products in their pipelines, they are increasingly focused on innovative products.

Of the companies with disclosed product pipelines, 53% have at least one clinical candidate with global first-in-class potential, meaning the candidate hits a target that isn’t hit by any marketed product of the same modality.

Fast followers are defined as companies with clinical assets against targets that saw first approvals in the last three years.

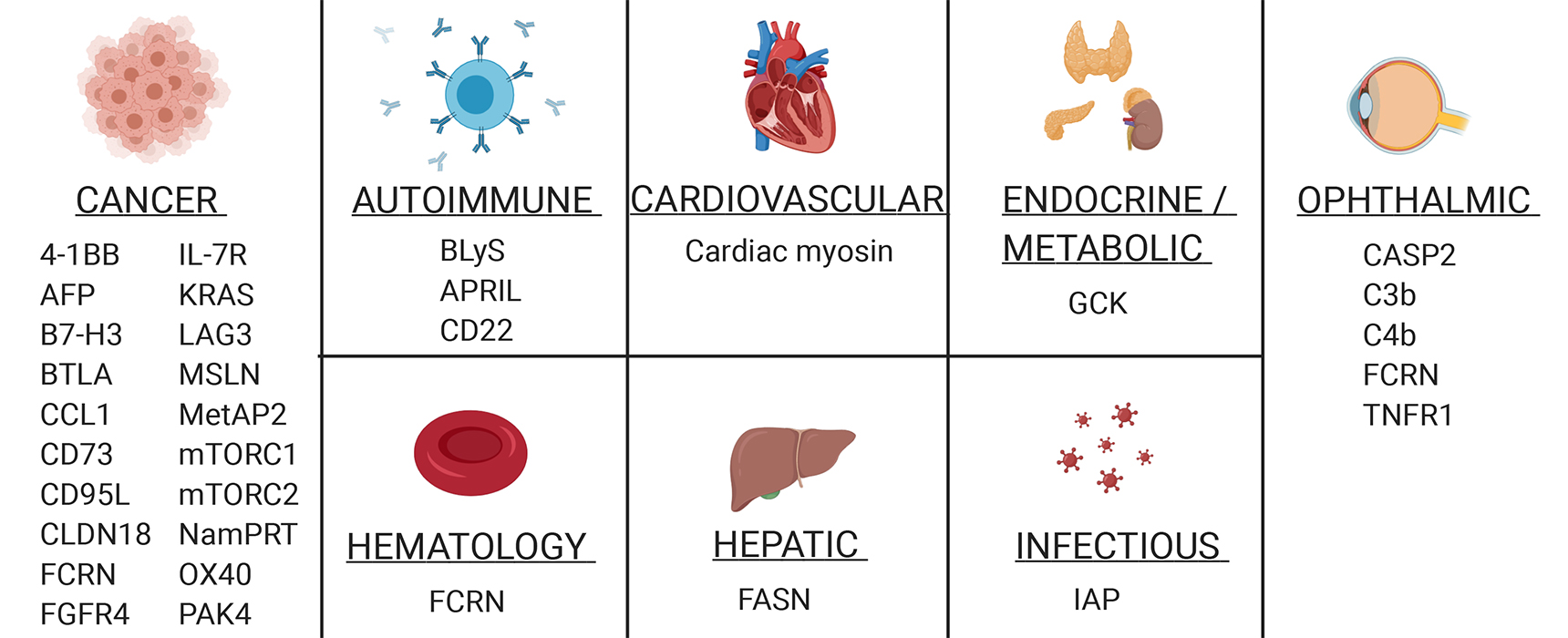

The potential first-in-class candidates in development at those 32 companies hit a total of 37 novel targets that haven’t been addressed by approved therapies of any modality, anywhere.

Cancer dominates the first-in-class targets, which is no surprise given the cancer-heavy focus of many Chinese biotechs, but the companies are also innovating on targets across a wide swath of other disease areas.

Avoiding platform risk

China’s top funded companies may be innovating on novel targets, but they generally aren’t showing the same level of investment in new modalities and technologies. Small molecules and standard mAbs remain the primary focus.

Among the twelve novel platform plays included in BioCentury’s analysis, half are focused on cell therapies, while the others span next-generation antibody technologies, nucleic acid therapies and gene editing technologies.

The investment trend in China stands in contrast to the U.S., where platform companies routinely draw venture rounds over $100 million and preclinical platform companies are filling the IPO queue.

In the U.S., 59% of the 22 therapeutics companies that have raised over $100 million in series A funding since 2014 are platform plays. Of those platform companies, 77% are working in cell and gene therapies.

The most recent platform success story may be the mRNA companies that have achieved platform validation through COVID-19 vaccines. Moderna Inc. (NASDAQ:MRNA) has seen a more than seven-fold increase in its share price since the beginning of the year.

Another example is CRISPR gene editing technology. CRISPR Therapeutics AG (NASDAQ:CRSP) is valued at over $10 billion after sharing early clinical data from just a few patients. The technology has also spawned a slew of next-generation gene editing companies that continue to attract top funding.

Chinese investors, however, are beginning to invest more modest amounts in platform technologies; many just haven’t reached the $100 million funding threshold for BioCentury’s analysis.

At least nine Chinese platform companies have received $25-$100 million in funding since 2014. These include biotechs developing cell and gene therapies, and those innovating around next-generation antibodies.

A notable example is Gracell Biotechnologies Co. Ltd., which is developing a suite of CAR T cell technologies including a rapid manufacturing platform, a dual antigen targeted approach and an allogeneic design.

The Chinese biotechs attracting the most funding are accessing a growing number of innovative products through licensing deals, but so far, few have taken on the risk of developing technology platforms in-house. That picture could soon change.

BioCentury’s analysis of the 97 Chinese biotechs that have raised over $100 million in venture funding or at least $100 million in an IPO since 2014 shows that most of these companies are innovating on targets rather than technologies. Only 12 are technology platform companies...